Are we back on track for good? It’s hard to say because despite the results we’ve seen since the beginning of the year, you may be surprised to learn that we’ve already had four rebounds of more than 6%between January 1 and July 31, 2022, including two of more than 10% (see chart below). The evolution of new data on different factors will determine whether or not the rebound can be sustained. Caution and patience are still required.

July 2022

- “Earnings season”: In my comment last month, I told you about the “earnings season” (the period when companies present their financial results for the last quarter) and said that it would have a significant impact on the direction of the markets in the coming weeks; And this is mainly what guided them during the month of July. As of August 3, 2022, 72% of the S&P 500 companies that have reported results have beaten market expectations (Source: Credit Suisse).

- Recession: I also mentioned last month a possible “technical” recession that would be announced in July; it came to fruition with the announcement of US GDP figures (an indicator of the US economy) which revealed two consecutive quarters of negative development. For the moment, this does not mean much since specific factors have contributed to these data. However, the evolution will be followed in the coming months because so far, although the majority of the figures released have been positive; The results were still contradictory at times. Consumers remained resilient despite extremely low sentiment indices, which supported the economy. Unemployment rates also remain at historic lows and the number of positions to be filled is declining.

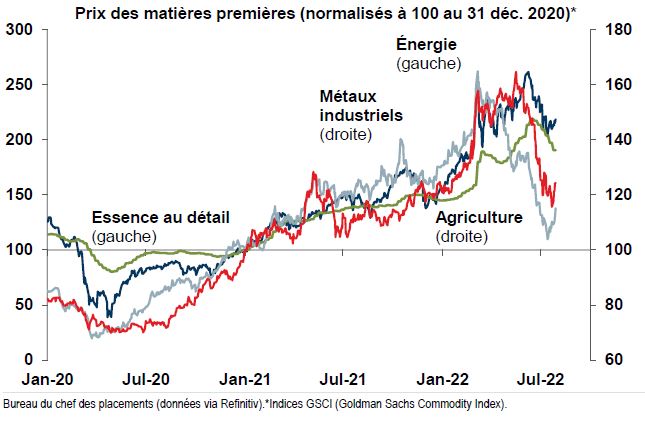

- Inflation: Also discussed in last month’s commentary, several positive signs related to inflation had begun to surface in recent months and expectations related to inflation decreased further in July. The United Nations Food Price Index was down in July for a4th consecutive month, now at a level below where it was before the invasion of Ukraine. Oil prices also continued their descent during the month, helping markets anticipate a decline in inflation in the coming months. Demand is also seeing a rapid shift from goods (televisions, appliances and other durable goods) to services (transportation, travel, hotels, restaurants, etc.); which helps to calm inflation on goods while supply chains regain the upper hand.

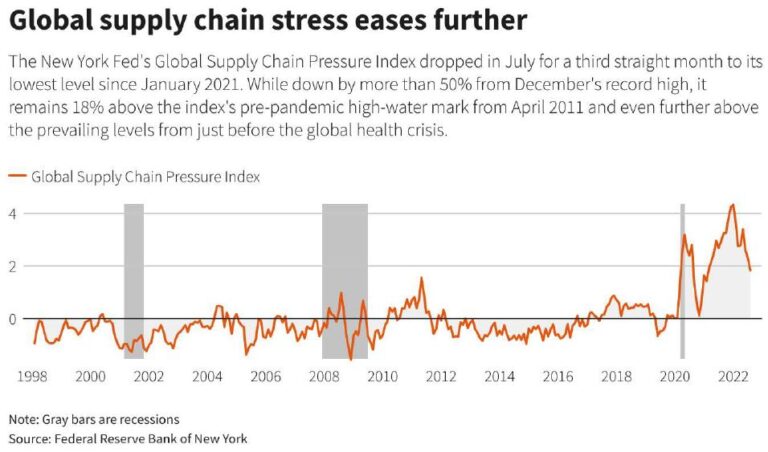

- Supply chains: The good news on this side has continued to improve on several points. Supply chain pressures continued to decline according to the New York Fed in July, now down more than 50% since December 2021 (a decline is positive here since it means a decrease in the pressures that cause problems). Delivery times also continued to improve during the month, according to the S&P Global and JP Morgan index that tracks these data.

Outlook for the coming months

July was a welcome month, which shows that good returns can often come at times when you don’t expect them. With the corporate earnings season now largely behind us, the other key points to watch for the coming months remain unchanged for now. The fine line between controlling inflation and recession is not straightforward and will continue to attract attention. We are going through a period where good news about the economy should not be too good, otherwise the risk of inflation increases; but also where good news on inflation must not be too good either, otherwise the risk of recession increases. I continue to believe that the chances of a severe recession remain low given the current labour shortage. Some sectors will be more impacted than others by the ongoing pressures. Technology companies that had thought too big during the pandemic and began to reduce the size of their workforce, with house prices skyrocketing due to very high demand and low interest rates; A return to normalcy in certain sectors would only be normal and possibly beneficial.

Strange as it may seem, recession fears helped markets have had a good July. Indeed, these fears have pushed interest rates down. A decline of this kind benefits both equities and bonds, which is part of the reason why both asset classes had a good month in tandem. Obviously, this factor must be coupled with others to produce positive returns such as the profits of companies that were there, lower inflation expectations, the state of supply chains that is improving, etc.

As in previous months, I continue to see positive signs in several sectors. However, as mentioned earlier, I believe that caution and patience are still required at this time since these signs will have to materialize and show a sustained trend before they can really be relied upon. Good diversification within portfolios is important in such markets.

What to watch for in August:

- August 4: Unemployment rate in the United States (result 3.5%)

- August 5: Unemployment rate in Canada (result 4.9%)

- August 10: U.S. inflation data

- August 16: Canadian inflation data

- August 25: Estimated U.S. GDP

- August 26: U.S. core inflation data

- August 30: U.S. Consumer Confidence

- August 31: Canadian GDP data

Please feel free if you have any questions/comments or would like to discuss them further.