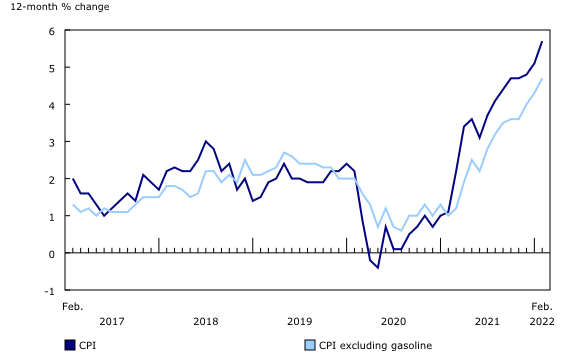

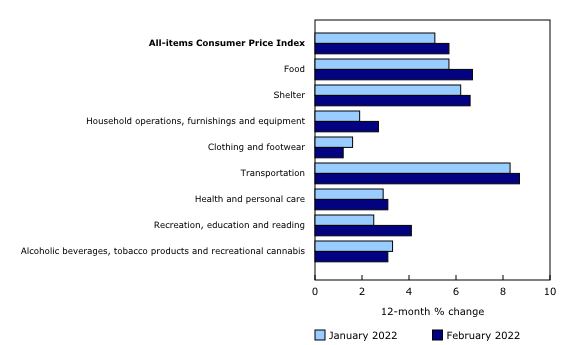

To start 2022, we were at the peak of the “wave” of the Omicron variant, financial markets had been on a rollercoaster since the end of 2021 and all eyes were now on inflation, central bank responses and what they would (or would not do) to calm the rise in consumer prices. Inflation reached 5.7% over twelve months in February 2022 according to Statistics Canada; And although price increases are widespread across all sectors, the price of gasoline has a lot to do with it since the increase, excluding the price of gasoline, was rather 4.7% over twelve months. These price increases, due in part to the reopening of economies around the world, supply chain problems, staff shortages and demand accumulated during lockdowns, are well above the Central Bank of Canada’s long-term inflation targets of 2% (range of 1-3%). In an environment like this, if they want to be able to calm the situation, central banks often turn to their tool of choice: interest rates.

1. Commentary on market volatility in the first quarter

The objective behind interest rate hikes is simple:

- Increasing the cost of consumer debt that will increase their fixed expenses

- Higher fixed expenses (mortgage, car, credit, etc.), so less money available for different products and services

- The balance between supply and demand; When demand decreases, prices will also fall

Take cars, for example; Currently, the inventory of new cars is very low. This leads to:

- Rising demand for used cars

- Low supply of used cars since people can’t have a new vehicle, so they don’t change

- Lots of demand, little supply and rising prices for used vehicles

Now let’s consider the same situation, but with higher interest rates. On the demand side, higher interest rates will mean that payments for the same car will be higher, but in addition, the consumer will have less money available since he already has to use more of his budget to cover his other expenses. Fewer people will want to switch under these circumstances and the demand for vehicles is reduced. On the supply side, manufacturers continue to produce new vehicles, individuals with leased vehicles will be able to exchange them more easily for new ones, and the supply of used vehicles is increasing. A decrease in demand, in this case coupled with an increase in supply, will cause used car prices to decrease. I agree that this is a greatly simplified scenario, but you understand what we are getting at.

It’s tempting to think that it’s simple and that we will easily solve it with interest rate hikes. However, we need to go a little further to understand the reality of the stock markets. The stock market is always trying, rightly or wrongly, to anticipate the future. While the scenario of raising rates to cool inflation seems rather simple and effective, it is not without risk. What would happen if central banks raised interest rates too much and too quickly? The fear of the financial markets in this case is, and this is by no means a prediction on my part, a recession. How could rate hikes lead to a recession?

- Higher cost of debt for consumers: lower demand for goods and services

- Decrease in revenue for businesses

- Higher cost of debt for businesses: lower profit margins and available money

- Weaker growth prospects for companies

- Employee cuts

This is one of the risks in the markets, but like the others, it is not certain to materialise. Central banks could be able to navigate to calm inflation without having a detrimental effect on the economy and this fear was then just a storm in a teacup. It will still have brought volatility to the markets.

This lengthy (but also brief) explanation mainly describes what was guiding the markets between the end of 2021 and the beginning of 2022. Unfortunately, for a portfolio of traditional equity and fixed income securities, this kind of scenario is negative, at least in the short term, for both sides.

- For equities, uncertainty and fear of adverse events will lead to volatility

- For fixed income, rate hikes will reduce the value of bonds since it has an inverse relationship with interest rate movements

Unfortunately, during the first quarter, there were very few places to hide to protect portfolios. Usually, when equities perform less, bonds compensate and vice versa. With the particular circumstances of the beginning of the year, this was not the case as the two moved in tandem. Quickly on the relationship between bonds and interest rates; You have an investment with a return of 3% per year and a new investment with the same risk and characteristics becomes available, but it will return 4% per year instead. Which one would you prefer? Let’s go back to the principle of supply and demand. People who are invested in the 3% investment will want to get rid of it and go for the 4% one. New investors will want to go straight to the 4% one. Therefore, the demand for the 3% investment will be low, which will cause its value to fall today (although the value at maturity remains the same). Again, this is oversimplified, but that’s the point. If you had answered prefer the placement at 3%, call me, we are due for a meeting.

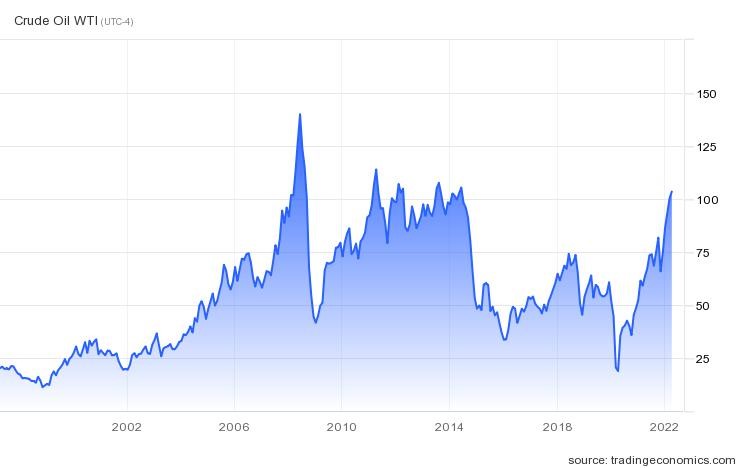

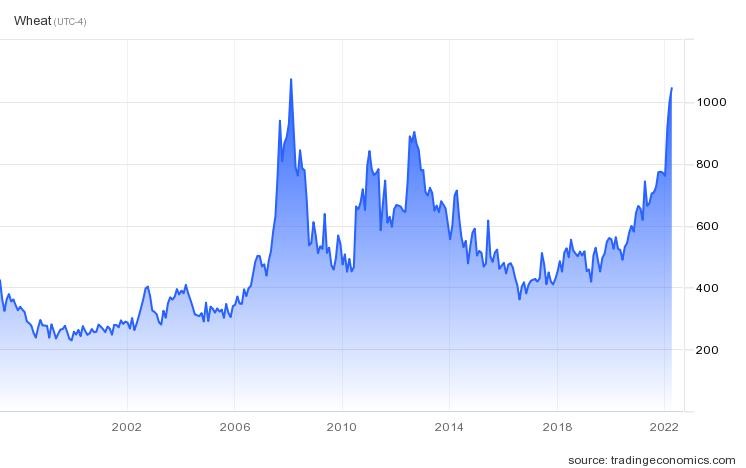

In February, rumors of an imminent Russian invasion of Ukraine were rapidly intensifying. On February 24, Russia began its invasion of Ukraine. This crisis is still unresolved, but as with many armed conflicts in the past, although they are terrible humanitarian tragedies, markets tend to be volatile in the short term and then recover. This time was no exception. Markets were volatile before recovering and attention returned to inflation management, which now had an additional pitfall in its way. Russia being a major exporter of several key products in the world (oil, natural gas, wheat, neon, metals, fertilizers, etc.), while Ukraine exported grain products, metals, etc.; This war further increases fears of persistent or rising inflation and this is what has led to sudden movements in commodities such as oil and wheat among others (see charts below).

2. Outlook for the coming months

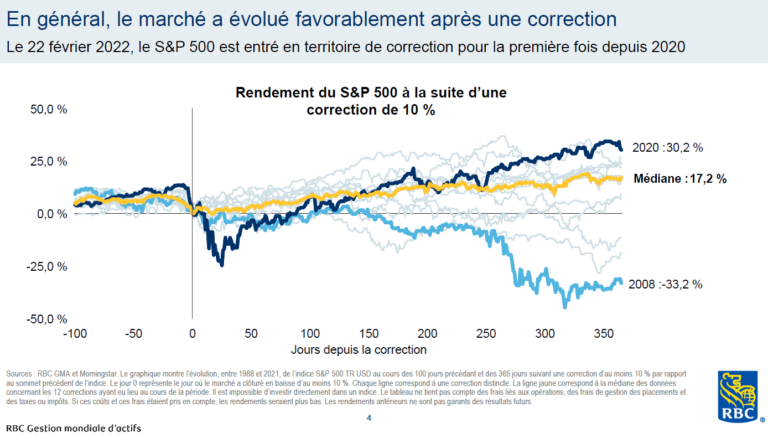

With this in mind, we start the rest of the year. The first quarter was not easy, but it served as a good reminder that financial markets are not just rising in the short term, despite what we have seen in recent years. These declines are never pleasant when you get through it, but they are opportunities to learn to live with the vagaries of the markets. The market declines by an average of 14% within a year, but it has still been positive in 32 of the last 42 (2nd chart). This learning will be useful when other difficult moments arise, because yes, there will be others. The important thing in these moments is to stay invested and keep the long-term goal in mind. We let the storm pass and we don’t panic because it’s not the first time, nor the last time; And we have learned from past experiences that this panic will not serve us at all. And if you ever panic and can’t do anything about it, you call your investment advisor. After all, that’s what he’s here for.

In the coming months, there will be a lot to look out for:

- Inflation developments

- Central bank activities

- Evolution of the conflict in Ukraine, which we all want to see a swift and peaceful resolution

- Covid-related changes are expected to become less important, but still need to be monitored

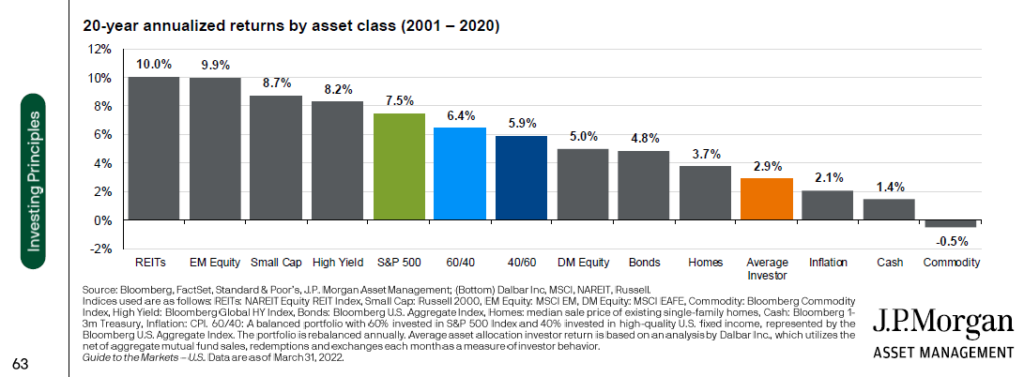

I expect volatile markets to persist and believe we will need to lower our expectations for future returns. The last few years have accustomed us to exceptional returns well above historical averages, especially in the U.S. market. For the next few years, and in the current context of high inflation, I think the exposure to Canada will be interesting. The Canadian market is favourable with oligopolies (think banks and telecommunications companies for example) and a significant weighting in the energy sector. The valuations of the companies are also much lower. Nevertheless, diversification will remain the key. It is essential to have a well-diversified investment portfolio since unexpected events will continue to occur and it is through good diversification that we will be prepared for multiple eventualities. Investment themes evolve and change over time and we will continue to adjust portfolios as needed. The table below shows the returns of different investments each year, showing that things can change a lot from year to year.

3. Final Words

You will find in the appendix below other interesting graphs on the effects of investors’ emotions on their returns and on the returns following market declines that I thought might be of interest to you. Forgive me for the English ones, they come from American companies and were therefore not available in French.

Of course, as I hope you all know, I remain at your disposal if necessary to answer your questions, fears, questions or other. Don’t hesitate, it’s always my pleasure to be there for you and that’s why I do this job. Plus, I have unlimited minutes on my phone!

Thank you for your trust.

ANNEX

Chart 1

The importance of staying invested. The average investor experiences significantly lower 20-year returns than a balanced portfolio, caused by behaviours that force them to enter when things are going well and exit when things are not going well.

Chart 2

Corrections (10% decline) often offer good investment opportunities.