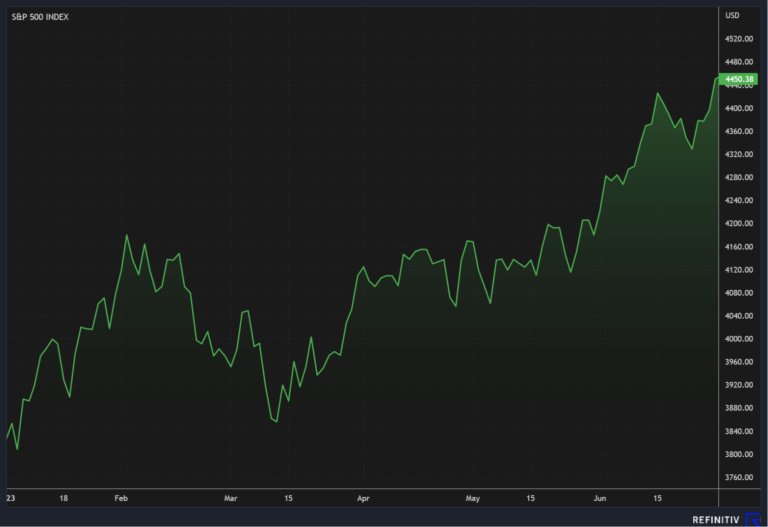

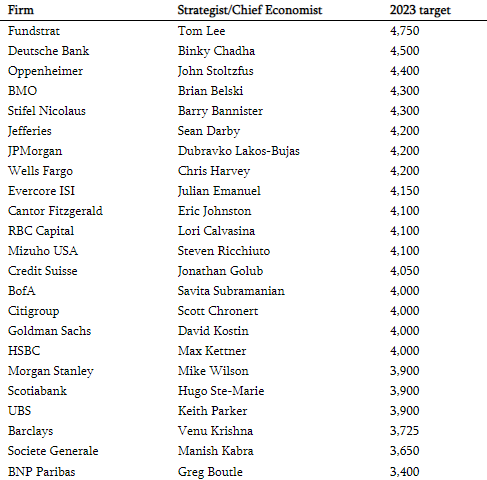

In the end, we have just had a very good first half of 2023. Looking at these results serves as a great reminder that no one can predict the direction of the markets accurately and that it is a dangerous game to attempt to do so. When looking at the forecasts of Wall Street strategists and economists at the end of 2022, many predicted a difficult first half of the year and a recovery in the second half of the year. JP Morgan, the largest US bank, forecast a return to the lowest level of 2022 in the first half of the year before seeing a recovery in the last 6 months. Bank of America, the2nd largest US bank, also forecast a difficult first half of the year before seeing a rebound in the second half. (Source) Closer to home, François Trahan declared on November 11, 2022 that the “economic apocalypse” was at our doorstep. However, the US stock market is up 11.46% between November 11, 2022 and June 30, 2023. Finally, the S&P 500 stock exchange, which includes the 500 largest companies in the United States, closed the first half of the year at 4450. For reference, here are the previously mentioned forecasts of the level at which the US stock market would end 2023 according to strategists from 23 of the world’s largest financial institutions. These forecasts were made at the end of last year.

That being said, even though we’ve been performing well for some time, that doesn’t mean it’s all behind us. There is still a lot of uncertainty in the economy and I think it is worth remaining cautious for the coming months. The markets are very optimistic and only the future will tell us if they are right to be so or not. Good diversification is still to be preferred. It’s often said, but good diversification with a long-term investment horizon is the best approach to take. The table below shows that each year, the sectors that perform best vary considerably. You will also note that often, the sectors that perform the worst over one period are often the best performers over the next. We have another good example of that so far this year; The top three performing sectorsbetween January 1 and June 30, 2023 were the worst performers in 2022 (communications services, information technology and consumer discretionary).

Interest rates

Interest rates have been talked about for almost 18 months now and they are still at the centre of economic and financial news. The effects of aggressive central bank rate hikes since last year are starting to be felt more and more by consumers, but the economy is still running well. The ideal “soft landing” scenario that central banks are aiming for seemed unlikely a few months ago, but the odds in favour of it seem to have increased lately as inflation slows in a resilient economy. The Bank of Canada recently raised its rate by another 0.25% to 5%; the Fed in the U.S. is likely set to do the same later this month.

Year-to-date performance

You may have heard that the good performance of the US stock market at the beginning of the year came mainly from some large companies that were driving the market up on their own. They have even been nicknamed “Magnificient 7”: Alphabet (Google), Apple, Meta Platforms (Facebook), Microsoft, Amazon, Nvidia and Tesla. This was true mainly until May, but the rebound widened to the rest of the markets during the month of June. There is now more depth at the restart. At the end of May, the Magnificient 7 was up 49.7% year-to-date and the other 493 companies in the S&P 500 were down 1.1%. Many companies were not participating in the rise in the markets, but the recovery has since become widespread. At the end of June, the 7 big tech companies were up 52%; But the other 493 were now up 5.1% year-to-date. Historically, it’s a good sign when more companies start to participate in the rebound.

May 31, 2023

June 31, 2023

Do not hesitate if you have any questions or would like to discuss them further.